Bonus depreciation is back in underwriting conversations, but investors are approaching it with far more discipline than during the last cycle. While the mechanics remain familiar, the more relevant question today is how the benefit should be weighed within pricing and underwriting decisions.

In the current market, bonus depreciation is less about creating incremental returns and more about identifying where it meaningfully enhances after-tax cash flow versus where it simply accelerates income that would otherwise be realized over time. As capital becomes more selective and assumptions tighten, investors are increasingly focused on when depreciation meaningfully improves outcomes and when it does not.

Who Actually Benefits

Bonus depreciation is driven by the characteristics of the asset itself, not by whether an investor qualifies as a real estate professional. Individuals, partnerships, family offices, and private investment groups may all benefit when acquiring qualifying, income-producing property that is placed in service properly.

In practice, the impact tends to be most pronounced for investors evaluating multiple acquisitions, operating through pass-through structures, or managing taxable income across portfolios. How depreciation losses are ultimately utilized depends on an investor’s broader tax situation and is best addressed with tax advisors. The depreciation potential itself begins with the property.

How Investors Are Using This Today

Today, bonus depreciation functions as one variable within underwriting, alongside interest rates, exit assumptions, and lease fundamentals. It can enhance early cash flow, but it does not change tenant credit, lease structure, or long-term demand.

As interest in tax efficiency has returned, some assets are already seeing pricing reflect anticipated depreciation benefits. Investors who assume full depreciation upside may find the benefit embedded in valuations. Those who underwrite it conservatively are better positioned to determine whether it improves risk-adjusted returns rather than simply pulling income forward.

Used thoughtfully, bonus depreciation can support broader portfolio-level tax planning. When relied on too heavily, it can mask underlying risk, a distinction that has become increasingly important in a higher-rate, more selective capital environment.

For investors evaluating retail acquisitions, bonus depreciation is best considered alongside asset selection and underwriting fundamentals. Retail properties with higher concentrations of improvements may offer opportunities for accelerated depreciation when paired with durable cash flow and disciplined pricing. Blue West Capital evaluates retail investment opportunities where these considerations may be relevant as part of the overall return profile.

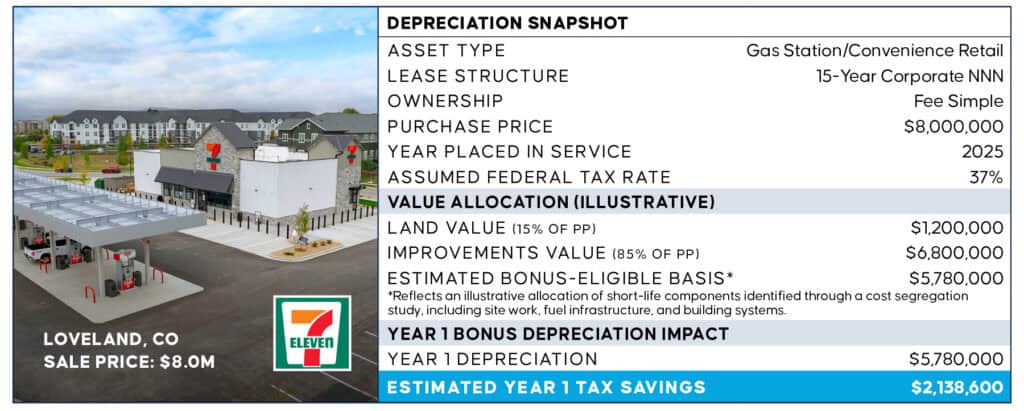

Bonus Depreciation Impact at a Glance

Case Study: 7-Eleven, Loveland, Colorado (Illustrative)

This case study is based on a recently completed, newly constructed single-tenant retail transaction represented by Blue West Capital. It is presented for illustrative purposes only and demonstrates how bonus depreciation may appear in practice for a high-improvement STNL retail asset.

Investor Insight: This example illustrates how a newly constructed, high-improvement net lease retail asset may generate substantial first-year depreciation and enhance early after-tax cash flow. The benefit is front-loaded and should be evaluated alongside hold period assumptions and potential depreciation recapture at exit.

Why Certain Retail Assets Show Up More Often

Certain retail property types surface more frequently in bonus depreciation discussions due to how value is typically allocated between land, building, and improvements.

Gas stations are a common example. A significant portion of value is often tied to fuel infrastructure and site work, including tanks, pumps, canopies, paving, and electrical systems, rather than the building shell. When properly analyzed through cost segregation, these components may qualify for accelerated depreciation.

Automotive-oriented uses such as car washes and lube centers often follow similar patterns. Their reliance on specialized equipment and mechanical systems can result in a higher concentration of short-life components. In many cases, 80 to 85 percent of total value may be attributable to improvements rather than land.

Importantly, these asset types are not inherently superior investments. The depreciation benefit is front-loaded and should be evaluated alongside hold-period assumptions, exit pricing, and potential recapture. Across retail categories, properties with specialized buildouts or equipment-heavy operations may generate meaningful depreciation, but only when supported by durable fundamentals.

A Familiar Tool in a Different Market

Investors have seen this cycle before. From 2017 through 2022, bonus depreciation played a major role in driving demand for newly constructed and improvement-heavy retail assets. Automotive-oriented uses in particular attracted capital due to their ability to front-load depreciation while delivering durable cash flow.

As bonus depreciation phased down beginning in 2023, its influence softened. The current reset restores the tax benefit, but under very different capital market conditions. Higher interest rates, more selective capital, and closer scrutiny of fundamentals mean bonus depreciation is once again a factor, but not a deciding one.

Information is provided for general informational purposes only and should not be relied upon as tax advice. Investors should consult their own tax and legal professionals regarding the applicability of bonus depreciation to any specific transaction.

As featured in Colorado Real Estate Journal.

Matt Lambright

Analyst, Blue West Capital

Be the first to know about new investment properties.

Subscribe to our mailing list