When purchasing commercial real estate investment properties, there are many variables and measurements that play a role in underwriting a property’s ability to generate cash flow. One crucial metric when financing is needed is the debt service coverage ratio or DSCR. In this article, we will break down debt service coverage ratios, the rise in interest rates, and the impact these are having on the ability for properties to be financed.

What does Debt Service Coverage Ratio (DSCR) mean?

Debt Service Coverage Ratio (DSCR) is a financial metric used by lenders to determine a borrower’s ability to service the debt. It is a ratio that compares a property’s annual net operating income (NOI) to the annual debt service. Lenders use DSCR to determine the maximum loan amount they are comfortable lending to investors when purchasing a property or to those refinancing.

The larger the DSCR ratio, the more income is available to service the debt. For commercial real estate investment properties, lenders typically have a minimum DSCR requirement of 1.25, indicating that the property generates enough income to cover the loan payments while leaving room for other potentially incurred expenses. However, not all lenders are created equal, and requirements vary depending on the bank, subject property, state of the economy, and the borrower.

How do you calculate Debt Service Coverage Ratio?

A property’s DSCR is calculated by taking a property’s annual Net Operating Income (NOI) and dividing that by the Annual Debt Service Payment, which should include both principal and interest payments.

The formula is:

Debt Service Coverage Ratio (DSCR) = Net Operating Income (NOI) / Debt Service

For example, if the property has an NOI of $125,000 with an annual debt payment of $100,000, then the DSCR is 1.25. Meaning the property generates more than enough income to service the debt payment.

Conversely, if the property has an NOI of $95,000 with an annual debt service of $100,000, then the DSCR is .95 and the property is not generating enough income to service the debt payment.

How do interest rates impact DSCR?

It is no surprise that as interest rates increase, so do annual mortgage payments. Therefore, to achieve DSCR requirements in today's lending climate, one of two things needs to happen: i) sale prices and returns need to be adjusted, or ii) the borrower needs to bring additional equity to the closing table. To truly understand how the rise in rates impacts property values and the ability to secure financing or refinancing, let's break down the Federal Funds Rate and what took place in 2022.

The Federal Funds Rate is the interest rate at which banks lend money to each other overnight. It is the most important interest rate in the U.S. economy and is set by the Federal Reserve. As the federal funds rate rises, banks pass additional interest costs to the consumer through higher interest rates. Lending spreads are a combination of treasury yield and risk spread over the treasury. Simply put - the higher the federal funds rate, the higher the interest rate for borrowers.

Given the recent headlines surrounding interest rates, it is easy to forget that the Federal Funds Rate was held at nearly zero in the first quarter of 2022. Since then, the Federal Reserve began tightening its monetary policy, and we have seen seven rate hikes increasing the Federal Funds Rate by a total of 425 bps over 10 months. The most recent rate increase occurred at the Federal Open Market Committee on December 14th, 2022, and increased the rate by 50bps for a federal funds rates of 4.25% to 4.50%.

What does the impact of rising interest rates look like?

To best illustrate the impact rising rates are having, let's look at an example of the same property being sold in today's market and compare that same property being sold one year ago. For this example, let's assume the property is a Single Tenant NNN investment with the following offering terms:

| Purchase Price | $5,000,000 |

| Cap Rate | 6.0% |

| Net Operating Income (NOI) | $300,000 (Purchase Price * Cap Rate) |

| Lender DSCR Requirement | Minimum of 1.25x |

With the information above, we can calculate the maximum allowable mortgage payment based on the net operating income and minimum DSCR requirement. This is calculated by dividing the NOI by the DSCR minimum ($300,000 / 1.25). The maximum annual debt payment for this property is equal to $240,000.

Next, we need to determine the maximum amount a lender will loan to the borrower, the "max loan amount." The max loan amount is calculated by using the following formula:

Max Loan Amount = 1 - PV(rate/12, amortization period*12, (NOI/12)/DSCR))

Let's look at how rates today differ from rates a year ago and its impact on the maximum loan amount:

Scenario 1: Lender DSCR Requirement in Today's Market

In today's lending market, interest rates are in the 6.25% – 7.25% range.

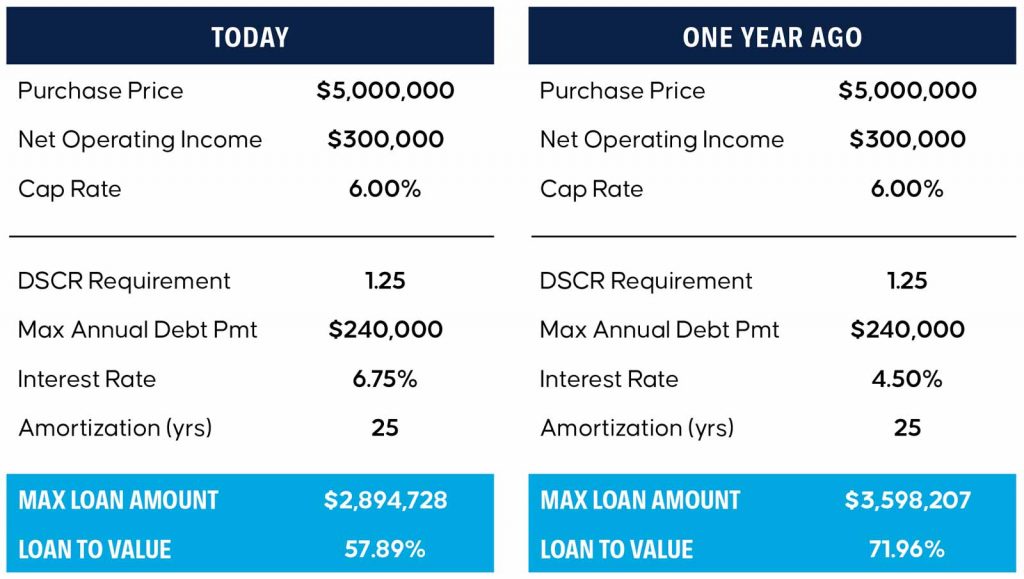

For this example, we assume a 6.75% interest rate with an amortization period of 25 years. This results in a Max Loan Amount of $2,895,728, which is a Loan to Value of 57.89%.

Scenario 2: Lender DSCR Requirement in Early 2022

In early 2022, interest rates were in the 4.0% – 5.00% range. For this example, we assume a 4.50% interest rate with an amortization period of 25 years. This results in a Max Loan Amount of $3,598,207, a Loan to Value of 71.96%.

Below is an illustration of the two scenarios mentioned above:

As evidenced by the illustration above, for the same deal to be financed today vs. one year ago, the borrower would be required to bring approximately $700,000 in additional equity to the closing table. That is equal to about 14.07% of the total purchase price.

That is one solution. The other would be for the sales price to adjust accordingly. To achieve a 1.25x DSCR with a more typical 70% Loan to Value using today's lending metrics, the purchase price would need to be $4,225,000 (15.50% decrease), which is a cap rate of 7.10%.

What does the rise in interest rates mean for property values?

It means that something must give. Rising interest rates have a considerable impact on assets that attract levered buyers. If the cost of debt is greater than the cost of equity (cap rate), the debt is considered 'negative leverage' and largely impacts returns. Unless pricing corrects, that trims the buyer pool to cash, or cash-heavy, investors. There was a time when all cash purchasers would secure more competitive pricing and slightly better returns. In today's market, the opposite is true. Investors are not naïve and will/have become more hesitant until pricing adjusts appropriately.

I understand that not all deals are created equal, and many other factors play into a property's ability to perform today and into the future. The rise in rates may be slightly muted if a property has a value-add component, a story of strong upside, and future rent growth. However, we use basic market assumptions to evaluate a general market trend and adjustment.

Lenders will maintain tight lending requirements through 2023 and the foreseeable future.

Many predict rates will increase in 2023 and will not come down, if they do at all, until 2024. As that continues, that puts direct pressure on cap rates and overall property values, to the tune of 10-20%, if not more significant. That is something that should not be overlooked.

Many hope a market adjustment will be shallow and that we'll rebound quickly. However, hope is not a strategy; every investor should have a comprehensive strategy in place as things shift. What does your strategy look like? Contact us today to discuss and customize a tailored plan.

Be the first to know about new investment properties.

Subscribe to our mailing list